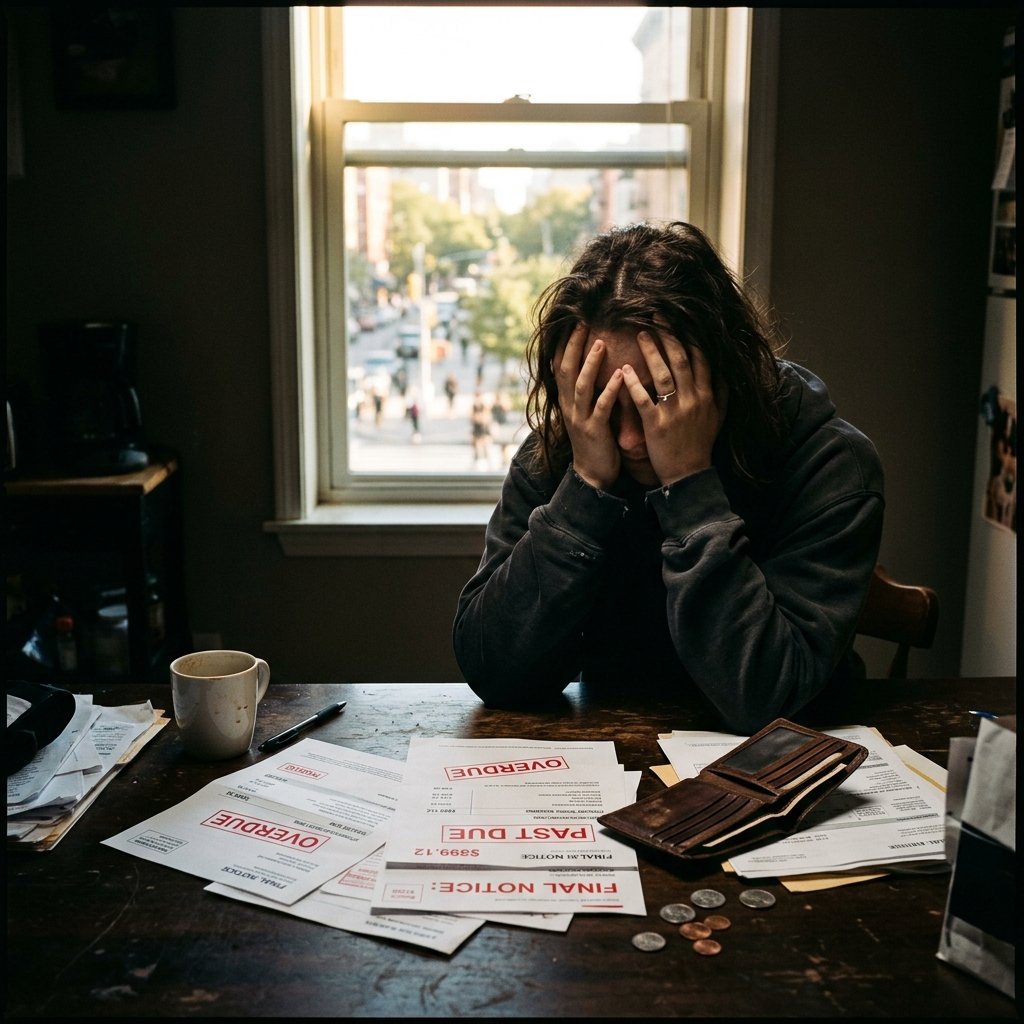

You have heard it a thousand times: “Think long-term.” “Play the long game.” “Invest in your future.” And every single time, you nod your head while a voice inside whispers: “That is nice, but I need to pay rent by Friday.”

Here is the truth nobody talks about: your inability to think long-term is not a character flaw. It is a neurological response to financial stress. Your brain is literally wired to prioritize immediate survival over future planning — and when you are broke, survival mode never turns off.

This article explains exactly why this happens, backed by actual research, and gives you a concrete five-step framework to override it — even if your bank account is near zero right now.

The Science: What Poverty Does to Your Brain

In 2013, researchers at Princeton and Harvard published a groundbreaking study in the journal Science. They found that financial scarcity reduces cognitive function by the equivalent of 13-14 IQ points. That is the same cognitive impact as losing an entire night of sleep.

Here is what happens inside your brain when you are broke:

- Your prefrontal cortex (future-planning center) gets overwhelmed. It is too busy solving today’s problems — how to cover the electric bill, whether to buy groceries or gas, which debt collector to ignore this week.

- Your amygdala (fear center) runs constantly. Financial stress triggers the same fight-or-flight response as physical danger. Your brain cannot distinguish between “a tiger is chasing me” and “I cannot make rent.”

- Bandwidth tax. Researchers call it “cognitive bandwidth.” When scarcity consumes your mental resources, you have less brainpower available for long-term decisions, planning, and self-control.

This is not laziness. This is not a lack of ambition. This is your brain doing exactly what it was designed to do — prioritize immediate threats over future opportunities.

The Scarcity Trap: Why Broke People Make “Bad” Decisions

Have you ever wondered why you bought something you could not afford, even though you “knew better”? Or why you took a payday loan despite understanding the interest rate was predatory?

This is the scarcity trap in action. When your brain is overloaded with immediate financial stress:

- You over-focus on today’s problem and literally cannot see next month’s consequences.

- You experience decision fatigue faster — every small financial choice (buy generic or brand?) drains the same limited cognitive pool.

- You seek instant relief — a $5 fast food meal feels more rewarding than a $5 savings deposit because your brain craves immediate escape from stress.

- You discount the future heavily — psychologists call this “temporal discounting.” The further away a reward is, the less value your stressed brain assigns to it.

None of these are moral failures. They are predictable neurological responses to scarcity. And once you understand the mechanism, you can start building workarounds.

The Exact Fix: A 5-Step Framework to Override Scarcity Thinking

You cannot fix the scarcity response by simply “trying harder” or “being more disciplined.” That approach uses the same prefrontal cortex that is already overtaxed. Instead, you need to reduce the load on your brain and create systems that bypass willpower entirely.

Step 1: Stabilize One Thing

Your brain panics because everything feels unstable. The fix is counterintuitive: do not try to fix everything at once. Pick the single biggest financial stressor and create a temporary solution.

- If rent is the crisis → call your landlord and negotiate a payment plan this week

- If debt collectors are calling → send a $25 payment to the loudest one to buy 30 days of silence

- If you cannot afford groceries → visit a food bank today (no shame, that is what they exist for)

Stabilizing one stressor frees up cognitive bandwidth for the next steps. You are not solving the whole problem — you are buying your brain enough peace to think clearly.

Step 2: Write Down the Chaos

Anxiety lives in the undefined. When your financial problems exist only in your head, your brain loops on them endlessly, consuming bandwidth 24 hours a day.

Get a piece of paper. Write down every single financial obligation, debt, and worry. All of it:

- Every bill and its due date

- Every debt and its minimum payment

- Your actual income after taxes

- Your actual necessary expenses

When it is on paper, your brain can stop holding it. This alone can reduce financial anxiety by 30-40%, according to cognitive behavioral therapy research.

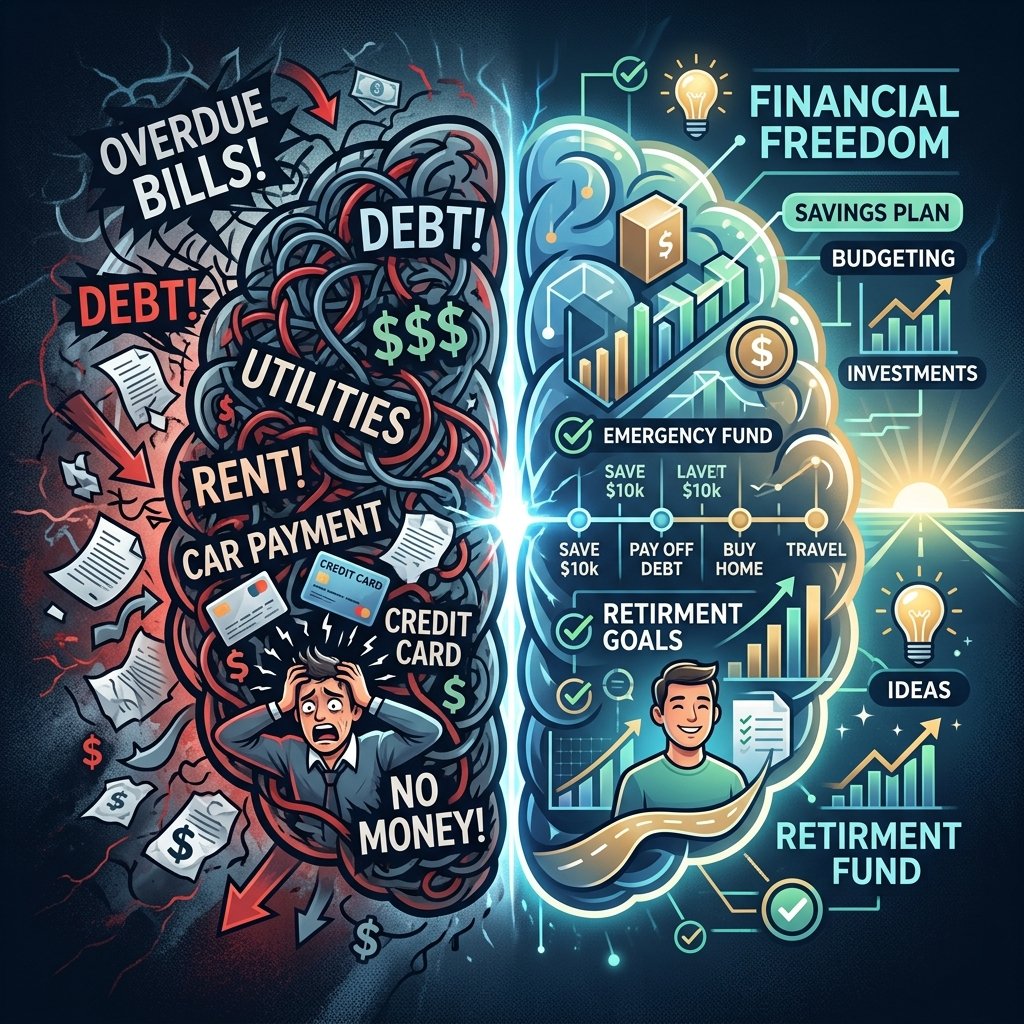

Step 3: Create a “Survival Budget” (Not a Dream Budget)

Most budget advice tells you to allocate money for savings, investments, and retirement. When you are broke, that is insulting. Instead, create a survival budget — the bare minimum you need to keep the lights on and food in your stomach.

Categories in your survival budget:

- Rent / Housing

- Utilities (electric, water, phone — minimum plans)

- Food (groceries only, no eating out)

- Transportation (to get to work and back)

- Minimum debt payments

Everything else is optional. Once you know your survival number, you know exactly how much income you need to simply stay afloat. Anything above that number is your escape fund — money you can use to break free from the cycle.

Step 4: Set One 90-Day Goal (Not a 5-Year Plan)

Long-term planning feels impossible because your brain cannot connect today’s actions to outcomes five years from now — especially under stress. The solution: shrink the timeline.

Set exactly one financial goal that you can achieve in 90 days:

- Save $500 emergency buffer

- Pay off one specific debt

- Earn $1,000 in side income

- Reduce monthly expenses by $200

Ninety days is close enough that your brain can visualize the outcome. It is long enough to make meaningful progress. And hitting that goal creates a psychological win that rewires your brain’s relationship with the future.

After you complete your 90-day goal, set another one. Stack them. In one year, you will have completed four 90-day sprints — and you will be in a completely different position than today.

Step 5: Protect Your Thinking Time

This is the step nobody tells you about. When every hour is consumed by work, commuting, chores, and stress, you have zero time to think about your future. And if you never think about it, you will never build it.

Block 30 minutes per week — just 30 minutes — for what I call a “Future Session.” No phone. No distractions. Just you and a notebook.

During your Future Session:

- Review your 90-day goal progress

- Identify one skill you could learn this week to increase your earning potential

- Write down one action you will take in the next 7 days to move forward

This single habit does more for long-term thinking than any motivational book or seminar. You are literally training your brain to look beyond today, 30 minutes at a time.

The Mindset Shift That Changes Everything

Here is what you need to understand at a fundamental level: you are not broken. Your brain is responding correctly to an incredibly difficult situation. The shame, the frustration, the feeling that you are “behind” — none of that is a reflection of your intelligence or your potential.

The difference between people who escape financial stress and people who do not is not talent or luck. It is this: the people who escape learn to work WITH their brain’s limitations instead of fighting against them.

- They do not rely on willpower — they build systems.

- They do not make 5-year plans — they stack 90-day sprints.

- They do not try to fix everything — they stabilize one thing at a time.

- They do not think their way out — they write their way out.

The Bottom Line

Being broke does not mean you cannot think about the future. It means your brain needs help to do it. Give it that help — stabilize one crisis, externalize your chaos onto paper, create a survival budget, set one 90-day goal, and protect 30 minutes a week for future thinking.

You are not stuck because you are not smart enough. You are stuck because your brain is spending all its energy keeping you alive today. Free up that energy, and watch what you are actually capable of.

Frequently Asked Questions

Q: Is “scarcity mindset” the same as being lazy?

A: Absolutely not. Scarcity mindset is a neurological response to resource limitation. It affects decision-making, planning, and self-control at a biological level. It has nothing to do with work ethic.

Q: How long does it take to shift from scarcity to abundance thinking?

A: Most people start noticing cognitive relief within 30-60 days of implementing the framework above. The key is consistently reducing financial stressors, one at a time.

Q: Can therapy help with financial stress?

A: Yes. Cognitive Behavioral Therapy (CBT) is particularly effective for financial anxiety. Many therapists offer sliding-scale fees, and some online platforms have sessions starting at $30-$60.